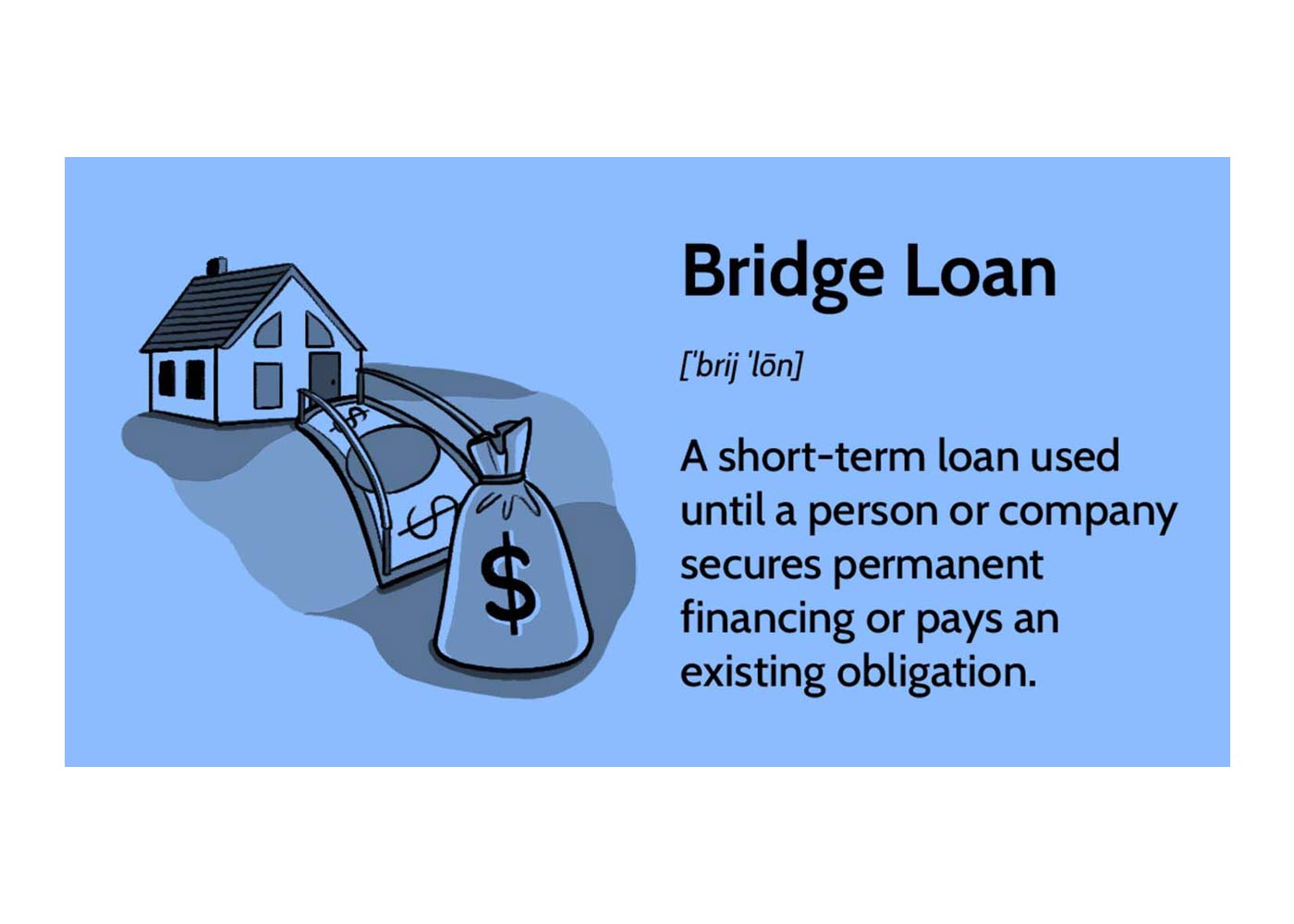

A bridging loan is a short-term loan secured by a property, similar to a mortgage. It functions similarly to a secured loan and is primarily interest-focused. Bridging loans are popular due to their fast application process and flexibility, with borrowers able to access funds quickly and use them for various purposes.

Different types of bridging loans are available across the UK, including commercial and residential bridging loans, and borrowers can easily choose one that better suits their needs. The number of bridging lenders and p2p lending platforms offering bridging finance has also increased, making it easier to find competitive rates.

You may be wondering why bridging loans are becoming popular; stay with us till the end to find the answer to your question.

How Do Bridging Loans Operate?

Bridging loans typically have a short repayment period, usually up to a maximum of eighteen months, although some lenders may offer longer terms. For first legal charge loans secured against property, the repayment period is usually limited to one year. However, this may not be true for second-charge bridging business loans.

The interest rate charged by P2P lending platforms is usually added to the loan and must be repaid at the end of the loan term. It is commonly known as rolled-up interest. Alternatively, borrowers may choose to pay the interest monthly, subject to providing evidence that they are capable of doing so

What Are Small Bridging Loans?

Small bridging loans can be obtained using unregulated properties or land, such as Buy to Let properties, commercial real estate, or land without planning permission, as first charge security. Alternatively, these loans can be secured as second charges on the above mentioned property types and commercial real estate for business purposes. These loans may also suit individuals with a high net worth and an annual income exceeding £150,000.

Bridging lenders can consider loan applications even if the applicant has a history of credit issues, and they may also evaluate loan requests without requiring proof of income. The loan agreement can be obtained quickly, and the lending process is generally smooth, with loans often granted promptly. P2P lending providers operating in the UK offer small bridging finance solutions.

How Can Small Businesses Benefit From Bridging Loans?

Small businesses benefit greatly from bridging loans as they offer a quick cash injection. Compared to other borrowing options, bridging loans require less stringent checks and can be obtained quickly. It makes them an affordable option with manageable repayment plans, depending on the exit strategy presented to the P2P lending platform. Bridging loans are especially helpful for individuals with small businesses.

P2P lending platforms can make fast and secure lending decisions, saving time on application processing. It is important to use a reputable P2P lending platform to expedite the process.

Why Should You Apply For A Bridging Loan?

Bridge finance is a convenient solution for individuals in need of quick cash. It is a short-term, interest-based loan designed to help during the transition, providing temporary financial relief. If you want to secure the loan, you provide your property as collateral.

Use A Bridging Loan For Commercial Real Estate

A commercial real estate mortgage is typically the preferred option for business executives looking to purchase a property. However, in certain unique circumstances, alternative solutions may be necessary.

When purchasing a property that requires extensive renovations or modifications, P2P lending platforms may suggest a property renovation bridging loan. Traditional lenders often do not allow significant changes to the property during the mortgage approval process, making a bridging loan a viable option for completing the necessary renovations. Once the improvements are complete, the bridging loan can be repaid by obtaining a traditional mortgage.

In addition, after completing property enhancements, the property's value is likely to increase, allowing for a larger loan amount at a lower interest rate.

Another scenario where bridging finance may be preferable is when a quick transaction is necessary. Commercial mortgage loans can be time-consuming and unsuitable for time-sensitive purchases, such as those made at auctions. Bridging finance is a viable option in these cases, particularly when there are issues with the mortgage application process.

P2P lending platforms offer bridging loans for land purchases, with a typical turnaround time of two weeks. These platforms provide competitive rates, with some exceeding their lending targets and achieving success in the market.

P2p Lenders And Bridging Loans

The term "small" in the context of loans usually refers to amounts ranging from £10,000 to £50,000. This loan category is gaining popularity among P2P lending platforms due to its rapid growth.

Leading P2P loan providers typically offer small bridging loans starting at around £18,000, with an average completion period of eight working days from the initial inquiry to full financing. These lending platforms handle all legal aspects of the loan process in-house, eliminating the need for borrowers to pay solicitor fees and expediting the loan approval process. It is a unique benefit not offered by other loan providers.

Conclusion

Bridging loans are becoming increasingly popular due to their flexibility, fast application process, and competitive rates offered by P2P lending platforms. Small bridging loans are gaining traction as they offer quick cash injections for individuals with high net worth, small businesses, and those seeking to purchase unregulated properties or land. With the lending process generally smooth and lending decisions made quickly, bridging loans are a viable solution for those seeking short-term financial relief. As such, using reputable P2P lending platforms is important when considering a bridging loan.

Share: